Dalberg uses cookies and related technologies to improve the way the site functions. A cookie is a text file that is stored on your device. We use these text files for functionality such as to analyze our traffic or to personalize content. You can easily control how we use cookies on your device by adjusting the settings below, and you may also change those settings at any time by visiting our privacy policy page.

In the developing world, more adults have bank accounts today than they had a decade ago. Yet much needs to be done in the area of financial inclusion as the use of financial products by women remains low. Dalberg Advisors Partner Naoko Koyama addresses this challenge in her talk as part of the Knowledge Seminar Series, held in collaboration with the Office of Development Affairs in Abu Dhabi.

The State of Financial Inclusion in the Developing World

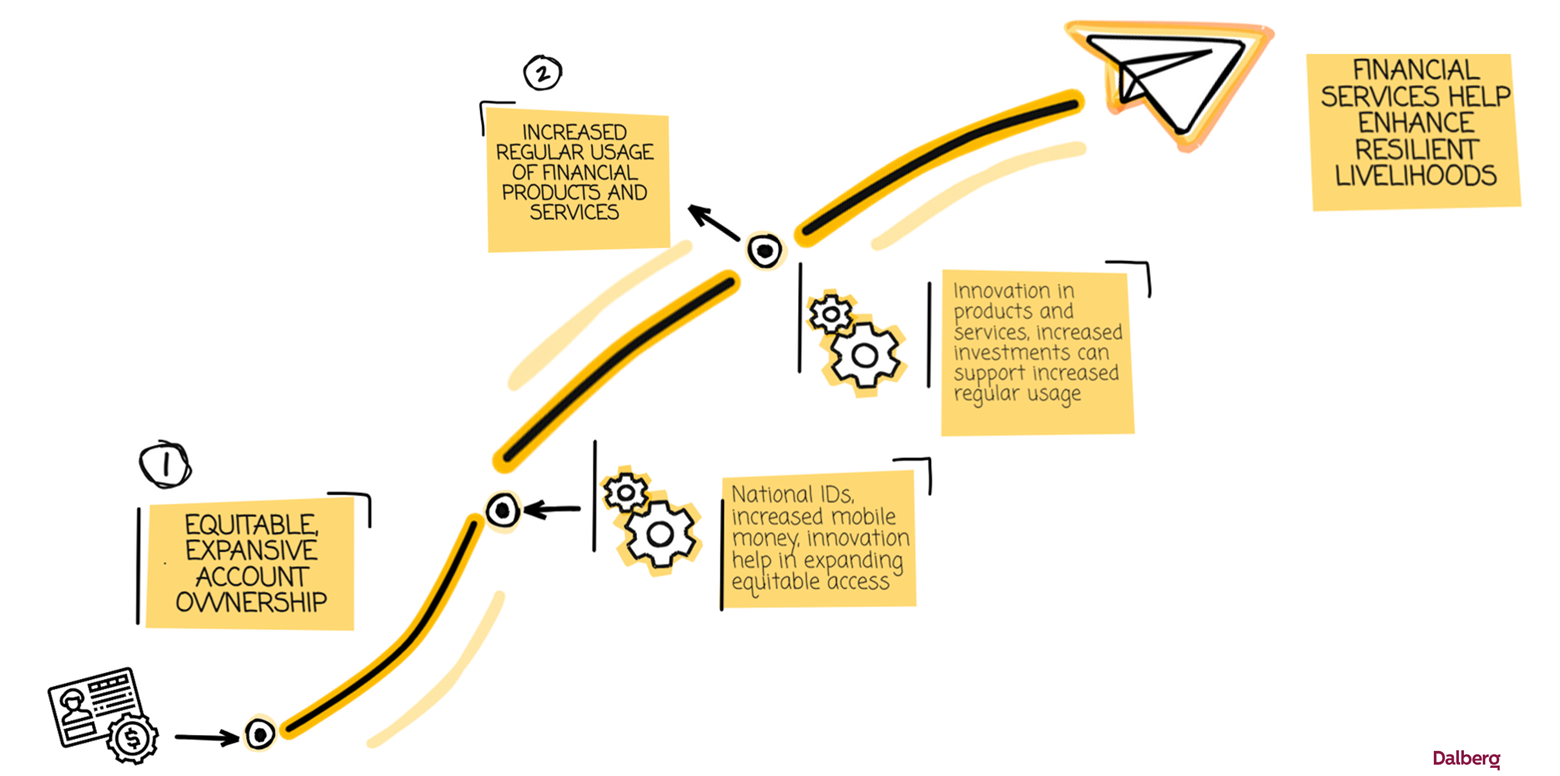

Financial inclusion is a journey that begins with a bank account. In 2011, 1.5 billion out of 3.7 billion adults in low- and middle-income countries had a bank account. Ten years later, that figure had doubled. Today, 71% of adults in developing countries have a bank account. However, the use of financial products is not as widespread. In Kenya, for example, while 80% of adults have bank accounts, only 20% have borrowed money from financial institutions.

Gender Inequity in Financial Inclusion

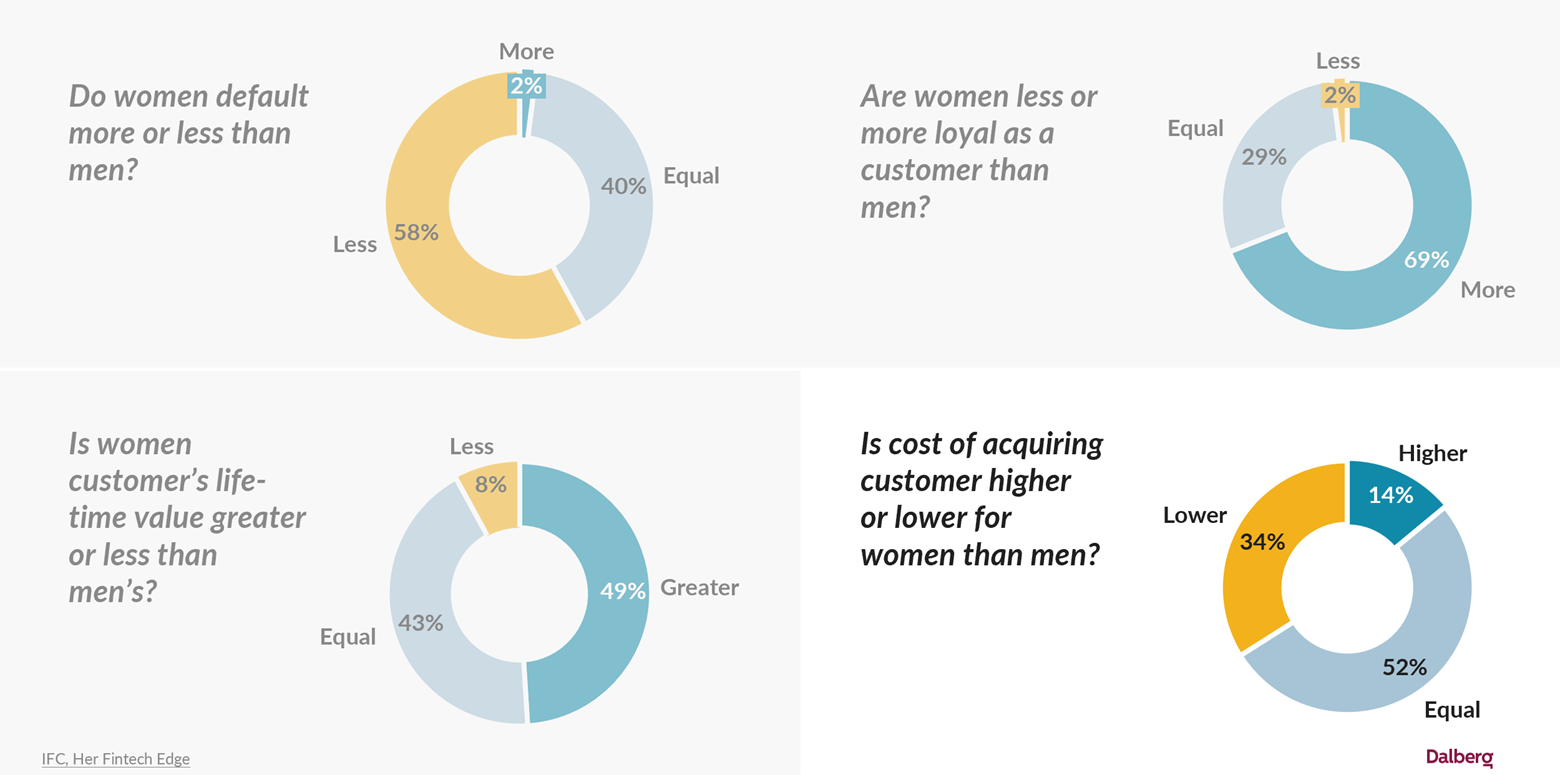

Women are less likely to have accounts or use financial products. To find out why, Dalberg interviewed 120 fintech companies in developing countries. The data showed that 63% of the companies said that only 25% of their business customers were led by women.

They admitted that women actually make better customers than men, but suggested that fintechs don’t necessarily understand what women want, or may find social norms difficult to negotiate, making investing in women not worth the effort. These are challenges that must be addressed. The other task is to unlock existing capital to make equity-driven investments.

Unlocking Existing Capital to Fix the Equity Gap

There are excellent examples of institutions that enable financing to women-led businesses such as Affirmative Finance Action for Women in Africa (AFAWA) and Ecobank. The efforts of such organizations help women take financial control of their lives.

Consider the case of Amina, whose life changed when her village in India was introduced to digital payment platforms. She was able to open a bank account and receive money securely. This prompted her to start a handicrafts business, a more reliable source of income than the informal jobs she had been doing. She was also able to acquire credit, network with other women entrepreneurs and leverage her connections to negotiate better prices.

By working with organizations committed to the cause of financial inclusion, Dalberg can ensure that women are better served.

Watch the video to know more about the gender gap in the financial inclusion space:

Watch the full version of the video here.