Dalberg uses cookies and related technologies to improve the way the site functions. A cookie is a text file that is stored on your device. We use these text files for functionality such as to analyze our traffic or to personalize content. You can easily control how we use cookies on your device by adjusting the settings below, and you may also change those settings at any time by visiting our privacy policy page.

With the recent announcement of free rations for 800 million Indians until November, the Indian Prime Minister took an important step in ensuring a basic level of food support for families that are struggling to make ends meet as the Covid-19 crisis unfolds. However, data clearly shows that much more needs to be done to safeguard vulnerable families through a health crisis that has become an economic catastrophe as well.

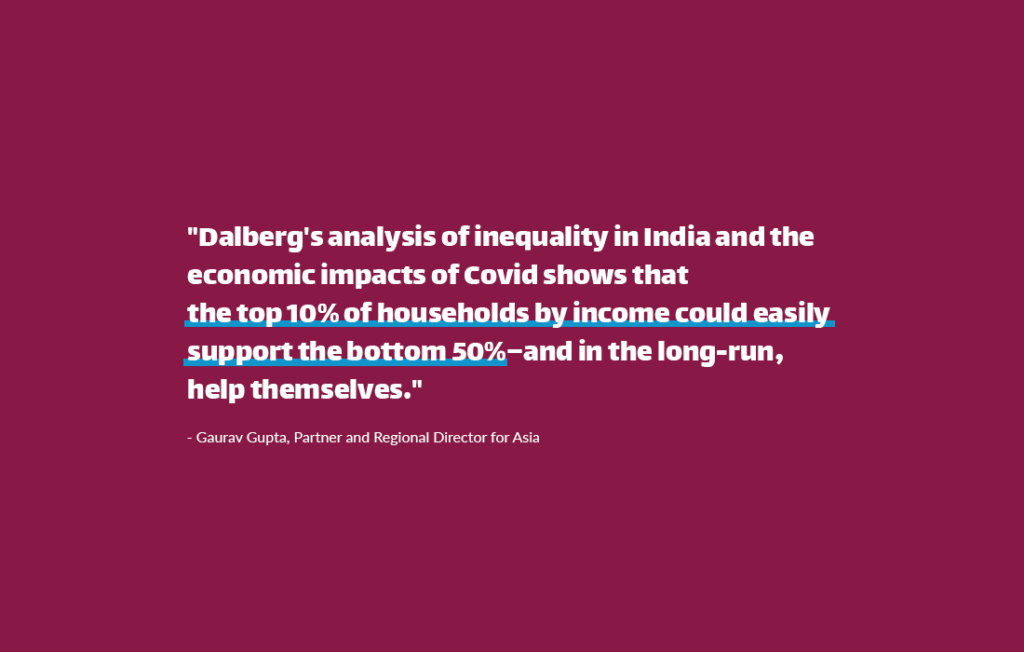

The government has limited room to manuever given budget constraints and declining revenues. But India’s true wealth has always resided with its citizens. We need to support each other and we easily can. Dalberg’s analysis of inequality in India and the economic impacts of Covid shows that the top 10% of households by income—those earning one lac ($1,400USD) a month and above—could easily support the bottom 50% households through this crisis—and in the long-run, help themselves.

The socioeconomic impacts of Covid on India today

The current Covid-19 pandemic has presented people around the globe with a common foe, but let that not lead us to think that we are all in this together. In the case of India, in the last 20 years, we have had the second highest rise in inequality in the world, second only to Russia. According to Oxfam, in just the last 12 months, the wealth of the top 1% in the country has increased by 39%, whereas the wealth of the bottom 50% increased by a dismal 3%.

India’s existing inequality has been compounded by the unequal impacts of the Covid crisis. Dalberg’s survey of 47,000 poor households shows the economic impacts have been devastating. Primary income earners in two-thirds of surveyed households have lost their jobs or wages. The average family has lost more than 60% of pre-crisis income and is now making just Rs. 4,000/month. 24% of low-income households have already run out of money and supplies. 40% of families have taken on debt, the poorest among them on average accumulating debt equivalent to a full month of their pre-crisis salary. In some States, as many as 1 in 5 primary income earners do not expect to find work in the future.

At the same time, the expenses for those in the bottom half are going up. A much higher percentage of the income of the poor is spent on basic essentials, which due to supply chain disruptions are rising in price. According to the latest RBI report, food inflation is again rising and hit 9.6% in June, driven mainly by vegetables, cereals, milk, pulses, edible oils and sugar.

Direct benefit transfers from the Central and State Government have helped—Dalberg’s survey suggests families received direct cash transfers of around Rs 2000 from the start of April to the end of May. But that represents less than 20% of monthly expenses. Many still fall between the cracks due to being left off government rolls.

As a result, the poor are being forced to take tough decisions. Do you cut nutritional intake? Do you avoid health expenditure? Do you remove children—most often girls—from school? These are the type of trade-offs that almost every family in the bottom 50% is considering.

Safeena Hussein, who runs Educate Girls, one of India’s largest frontline NGOs helping put children back into school, summarizes the challenges well: “Our biggest concern is that as families get used to seeing their daughters back collecting water, cooking cleaning, tending goats, etc. School will become a distant memory for them again and re-enrollment will be impossible against a backdrop of increased economic hardship. We have seen this in past economic shocks.” Such forced hardships will mean the poor will not only emerge poorer—for many, the impacts will reverberate far into the future.

Why the rich should act as insurance for the poor

However, what if we see our deep inequality as an opportunity to insure each other in this time of crisis? The richest 10% of households have an average monthly income of 2.9 lacs a month ($4,000 USD). Families in the poorest 50% of households have an average monthly expenditure of Rs 7,000 ($96 USD). Given the length of the crisis, let us say we provided for 3 months of monthly expenses for every family in the poorest 50%—that is only 3% of average annual income for rich households.

What if the lens is switched from income to wealth? In the case of wealth, only ~0.4% of the wealth of the richest 10% of families would need to fund the poorest 50% through this crisis. With such levels of inequality, the moral imperative is clear.

There is also clear self interest for why the rich should act as insurance for the poor. Trickle-down economics hasn’t worked, but trickle-up economics does. Any transfer of income to the poor during this moment of crisis comes straight back as extra consumption. Contrast this with retaining additional income with the rich where a much higher percentage will be saved—exactly the opposite of what the economy needs right now.

Transfers to the poor also mean savings on health, law and order and welfare costs. All of these things drive growth—the magic ingredient driving valuations of the wealth that rich people hold. Theoretically, we would be making these optimal transfers through tax collections that subsequently are transferred to the poor by government. But with the immediacy of the crisis, the government is highly constrained by fiscal pressures, and less than 2% of adults pay taxes. Raising taxes would only punish those that are actually taking part in the system and potentially depress investment. Widening and improving the tax base is an imperative, but is a long game at odds with this immediate crisis.

A transfer system is close at hand

The good news is that government has been reasonably successful in laying the rails for getting money to poor households, thanks to a host of digital and physical financial infrastructure. It is not perfect, but through a combination of government and NGO data, it is possible to know who these poor households are and what bank account they are linked to—acknowledging that there is still a sizable minority that is left out.

To date, we have been focused on the government’s use of these rails. What about if they were used by citizens for a citizen-to-citizen transfer? Some NGOs and funding platforms, such as Give India, are already creating such opportunities, and channeling money directly into beneficiary accounts. These efforts point the way to a larger opportunity to create a scaled platform for direct citizen to citizen giving.

What if there was a central clearing house that accepted money in any form (even cash for all those non-tax payers) and then transferred it directly into the accounts of the poor? This could act as a kind of Citizens Care Fund, with no government involvement and no concerns about leakage.

Building it is not hard—believing people will give is the real question. So whether out of a moral imperative or self-interest, are we willing to pledge to transfer 3% of our income this year to families in need? It’s a relatively small amount, but transformative for poor families. Could such a pledge be a movement? Like marked fingers on voting days, could this commitment become the new bragging rights amongst the rich?

Make no mistake, the wealthy are not going to save us. Those helping us survive this pandemic are those who carry on farming, continue to deliver goods, provide essential social services, keep law and order, and place themselves on the frontline of health work. Very few of them are in the top 10% of earners. It has been heart-breaking to see the pandemic exacerbate the already crippling burden of inequality on this country and to know that worse may come. By stepping up to provide some insurance to those in need at a time of unprecedented crisis, the wealthy have a chance to use some inequality for good—it is our imperative as citizens.

Gaurav Gupta is a Partner at Dalberg and Regional Director for Asia.